Sheila Oliver's Campaigning Website

Main menu

- Home Page

- Contact me

- Dedication

- Online Safety

- Online Safety 2

- Contract Law

- People with disabilities

- Drug and Alcohol Abuse Help

- Alan Dransfield

- Robert Pickthall RIP

- Luba Macpherson

- Nina's Story

- Padden Brook vexatious to mention it. Corruption again?

- Tales from a 4* Council

-

Dodgy LibDems Mr Parnell RIP

- Mr Parnell RIP

- Town Hall Protester

- SMBC CCTV evidence

- Council taxpayer sworn at by council employee

- Kick football supporters heads in

- Security guard slaps manager

- If I beat you up

- Arrested for trying to report a Data Protection Offence

- You piece of sh*t

- John Derbyshire, CPS

- No assault with a sneeze and they all knew that

- Can't even cross town for a medical appointment

- Arrested for using the town hall loo

- Punished, even though innocent

- Mr Parnell's simple problems

- Custodies, arrests, imprisonment 1

- Tagged but innocent

- Begging to have tag removed for Christmas Day

- Mr Parnell's Genius

- Why did no-one stop this lunacy?

- Goddard

- Lord Goddard stops him protesting

- Goddard breaches Data Protection Act

- Inmate!

- Begging Stockport Council for help

- My attempts to stop them

- Suicide attempt

- Snowpatrol and Mr Parnell

- Arrested 2/12/08 for assault

- Still under house arrest November 2009

- Custody in Cheadle Heath Police Station

- Still on bail Jan 2010

- Court refund/cheque

- GM Police & Crime Commissioner

- Police interview ref 1052176

- Aquitted Jan 2010 but still on bail Jan 2013

- Stop and Search 26/06/09

- Police refusal to disclose

- Chief Constable Fahy

- Stockport CPS fit for purpose?

-

Dodgy LibDems Toxic School

- Toxic Waste Dump School

- £multi-m planning fraud

- Culprits of multi £m fraud

- Rise in cost £5.5m to £7.5m in 2 months

- 5 months later cost is £8.2m

- Cost rise from £5.5 to £10m over 2 pages

- Cost now £10m

- £5.5 to £10m

- Donna Sager was telling me everything was fine; it wasn't

- Obvious concern over funding

- £6.9m to come from sale of redundant school land; oops, no it isn't

- Missing £201,750?

- Goddard covering up

- Another £5m anomaly

- Cheaper, larger school in 2014

- Goddard's lies

- Rising school costs

- Shortfall gone - how?

- Why no public Inquiry?

- Still paying architects - why?

- Financial Irregularities

- Anti-fraud policy (ha ha)

- Covering up LibDem fraud

- Concealing Contamination

- Hiding contamination

- Trying not to investigate

- Contamination 1

- Contamination 4

- 50% toxic hotspots

- Sister site evacuated July 2012

- Lying about having complied with BS10175

- £10m school too small

- Drainage problems

- Who trousered the £200k?

- Traffic

- How did it pass planning?

- Loss of Public Open Space

- No playing fields

- Miscellaneous Shenanigans 1

- Miscellaneous Shenanigans 2

- Dodgy LibDems A6 MARR

- Dodgy LibDems Offerton

-

Dodgy LibDems General

- Cancel meeting to go electioneering

- Sue Derbyshire

- Failure to oversee costs another £5m

- Junction 25 Recycling Centre site

- "Ragbag" local paper

- Windlehurst Park

- Andrew Webb

- Cllr Iain Roberts tries to block free speech

- Coach Park, Cheadle Hulme on Green Belt - Why?

- Banned council taxpayers

- Bridgefield Development

- Council Bad Practice

- Councillors, bless 'em

- Councillors should be doing this

- Council Bad Practice

- Residents Parking Scheme

- Portas Pilot Stockport

- Alice Through The Broken Glass

- Grand Central

- Bredbury Pollution and Fire incident

- Dodgy LibDems - Blackstone

- LibDem Councillors

- Dodgy LibDems Aquinas College

- LibDem FOIA/EIR 2004 abuses

- Dodgy LibDems Sandringham Road

- Arms' Length NPS

- Stockport Council wasting money

-

Cheshire East Council - Shenanigans

- Situation June 2016

- Silk St Development

- Silk St Development - abuses?

- Bryn Higgott, a Cheshire East solicitor

- A going concern? Of course it was.

- Yet another development scheme

- Make it Macclesfield

- Cllr Hilda Gaddu

- Heads of Terms

- CEC - further police investigations

- Anwar Majothi

- Bredbury Hall Hotel

- De Vere Hotels

- Disability problems compounded

- Dodd Group

- Dragonfly Environmental Ltd

- Drivas Jonas

- GVA Grimley

- Hantall Developments

- Jackson, Jackson & Sons

- Jackson Lloyd Ltd

- Life Leisure

- M60 Denton to Middleton Section

- Mr Stunell and Mr Hunter LibDem MPs

- North Reddish Labour Councillors

- Re-open the Woodhead Tunnel

- Stockport Grammar Extension

- Tee Hee

- Village Hotels

- DRANSFIELD

- DEVON

- DORSET

- GENERAL

- Dumfries and Galloway Council

- Berwick Town Council

- Salford

- Manchester

- Docs school

- Docs school 2

- Docs school contamination

- Docs Parnell Council

- Docs Parnell Stunell

- Docs Parnell police

- Docs Trident Foams

- Docs ICO

- Docs general

- Docs council officers

- Docs LibDems

- Docs Grand Central

- Docs bypass

- Docs Norse

- Docs Offerton Precinct

- Docs St Peter's Square

- Docs Offerton in General

- Docs Woodford

- Docs Blackstone

- Docs Aquinas

- Photos

- Toxic Waste Dump School

- £multi-m planning fraud

- Culprits of multi £m fraud

- Rise in cost £5.5m to £7.5m in 2 months

- 5 months later cost is £8.2m

- Cost rise from £5.5 to £10m over 2 pages

- Cost now £10m

- £5.5 to £10m

- Donna Sager was telling me everything was fine; it wasn't

- Obvious concern over funding

- £6.9m to come from sale of redundant school land; oops, no it isn't

- Missing £201,750?

- Goddard covering up

- Another £5m anomaly

- Cheaper, larger school in 2014

- Goddard's lies

- Rising school costs

- Shortfall gone - how?

- Why no public Inquiry?

- Still paying architects - why?

- Financial Irregularities

- Anti-fraud policy (ha ha)

- Covering up LibDem fraud

- Concealing Contamination

- Hiding contamination

- Trying not to investigate

- Contamination 1

- Contamination 4

- 50% toxic hotspots

- Sister site evacuated July 2012

- Lying about having complied with BS10175

- £10m school too small

- Drainage problems

- Who trousered the £200k?

- Traffic

- How did it pass planning?

- Loss of Public Open Space

- No playing fields

- Miscellaneous Shenanigans 1

- Miscellaneous Shenanigans 2

- Footpath diversion

- Snoozing watch-pussycats

- Anwar Majothi

- foi abuses

- foi campaigner

- Blocking Information

- Derbyshire won't answer

- Vexatious

- Compulsory Purchase Order of land

- Tender document

- Village Green

- Culprits

- Why LibDem Stunell shouldn't get a peerage

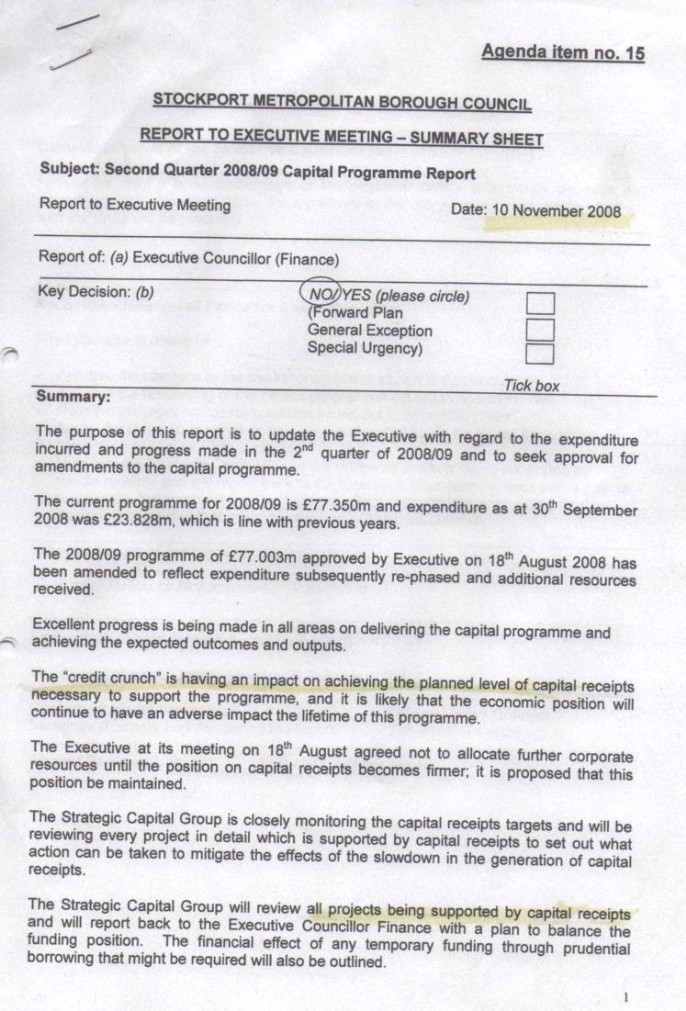

Financial Irregularities 2

5/10/05

The premises to cost overall £5,500,000

To be funded from DfSE grants 45% 2,475,000

Balance from Council's capital programme 55% 3,025,000

5,500,000

No mention here of the future of the existing schools and the land. Was the £3,025,000 capital programme to be a completeley fresh section of the programme or was the sale of the Fir Tree etc seen on the horizon?

12/12/05

Review -

Plus external works 444,000

Abnormal foundations (piling) 100,000

Drainage 133,000

Prelim external works 145,000

Services -

Contingencies 318,000

Other "property services" 550,000 (Wow! NPS rides again)

Planning, consult, Topo 82,000

Total £7,503,000

Funding shortfall will lead to ultimate failure of the project if not addressed -

Concern is expressed over funding! Donna Sager to look at other sources.

Look backwards again. Having been seemingly unaware of the monumental costs not considered in the first place (5/10/05), does it not now put in doubt the decision that refurbishing was not a way to go and not impractical?

22/03/2008

Now the total cost is £9,930,000

How has the funding been made available?

supported borrowing £2,902,000

allocations (not specified) 259,000

capital receipts 6,679,000

£9,840,000

Error in adding total but irrelevant 90,000

Total £9,930,000

In any event, the Finance Director under some pressure produced an explanation (at least a partial one) of the increase to £9,930,000. From £5.5 million to £7.5 million and then £8,5 million in a short space of time. His assistant wrote to us naming no less than 6 funds being accessed -

Cost £8.5 million -

grants 2,744,430

council -

capital receipts 1,676,000

£8,500,000

The Council added £768,431 and fees/costs to the lowest tender to meet the £8,500,000.

But, costs have now risen.

Project Executive -

Surveys have revealed arsenic levels which are high and have to be removed.

Brown asbestos is present -

Is this really the same scheme as described in the 05/10/2005 statutory proposal -

Analysis of the £6,679,000 is vital to put the jigsaw together -

Is there any connection between any of the buyers (or their agents) of Fir Tree, Taxal, Edgeley and the contractors (lowest tender)?

The higher costs include

Increased floor area £1,330,000

Planning 590,000

Inflation to 2009 1,140,000

The inflation calculation does seem high but I am not allowed to ask details of the calculation -

What invoices were used. The costs are very much towards the end of the project.

How did Donna Sager comply with the Prince 2 accounting system with the Schweinerie documented above?

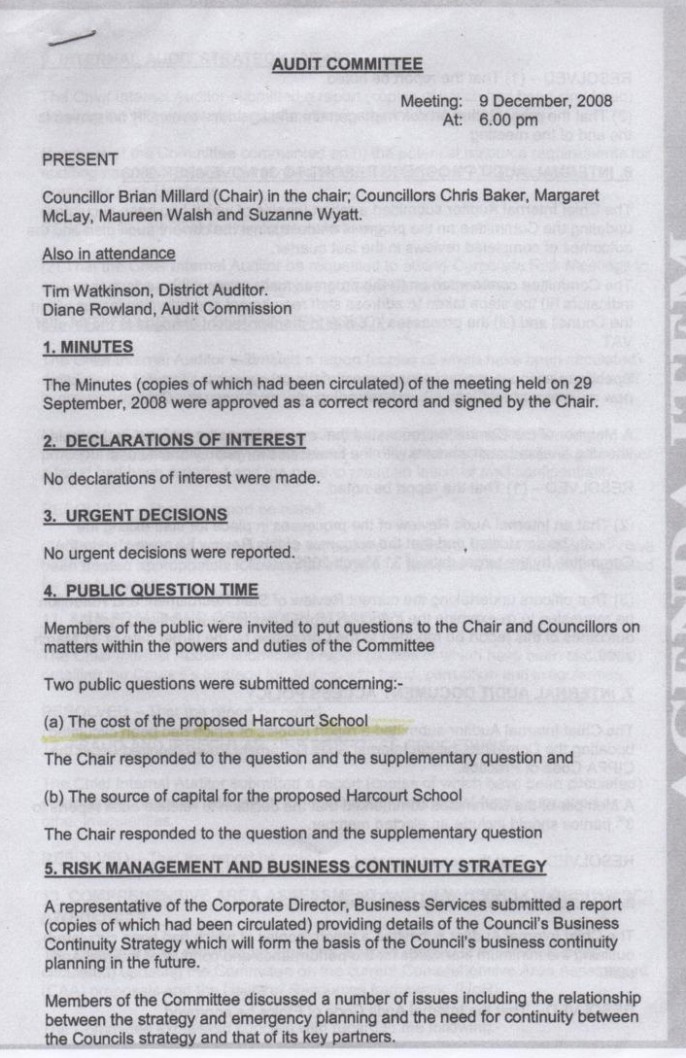

All these financial issues were raised with the Audit Committee to no avail. What is the point of the Audit Committee? They were useless with regards to SK Solutions too:-

http://www.sheilaoliver.org/sk-

I attended council meetings. I knew the sale of redundant school land was not making the sums they expected. That was how they intended to pay for the toxic waste dump school. How are you going to pay for it? I asked. Don't be vexatious, they replied -

They spent the money originally given by the Government for the new school on the other projects above.

Is Rachel Rosewell fit to hold the position she does if rises from £5.5 million to £9.94 million don't cause her to turn a hair?

Public Bodies Corrupt Practices Act 1889

I wonder what this payment was for? No doubt it will be "vexatious" of me to ask.

CHILDRENS & EDUCATIONAL SERVICES PREMISES RELATED Mar-

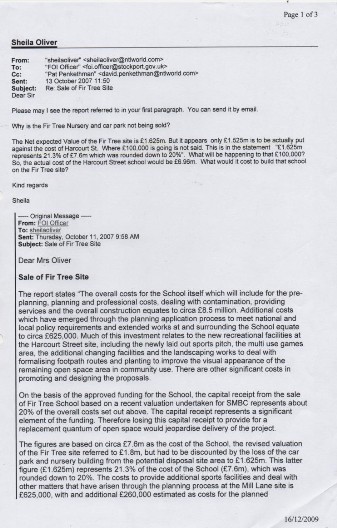

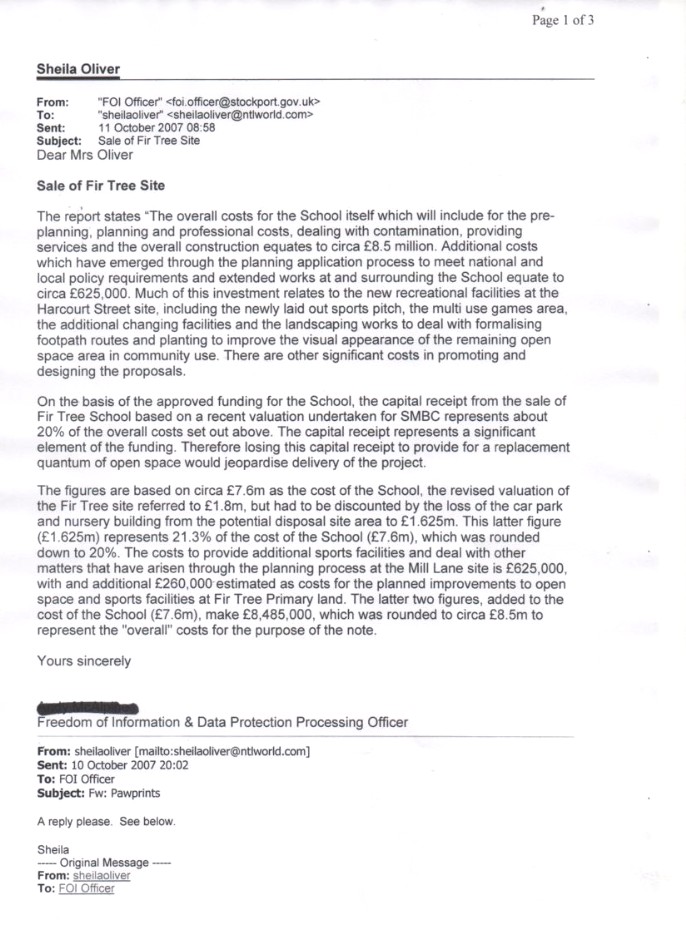

“The overall costs for the School itself which will include for the pre-

Therefore there are no specific costs regarding removing ‘toxic waste’ but the estimate of £8.5 Million for the costs of the school includes the costs of implementing the recommendations of GMGU. The exact costs of the recommendations have not been separated from the overall estimate of the scheme. It should be noted that it is impossible to give actual costs for individual elements of construction of the school but as the detail designs develop, so will the estimate of the costs."

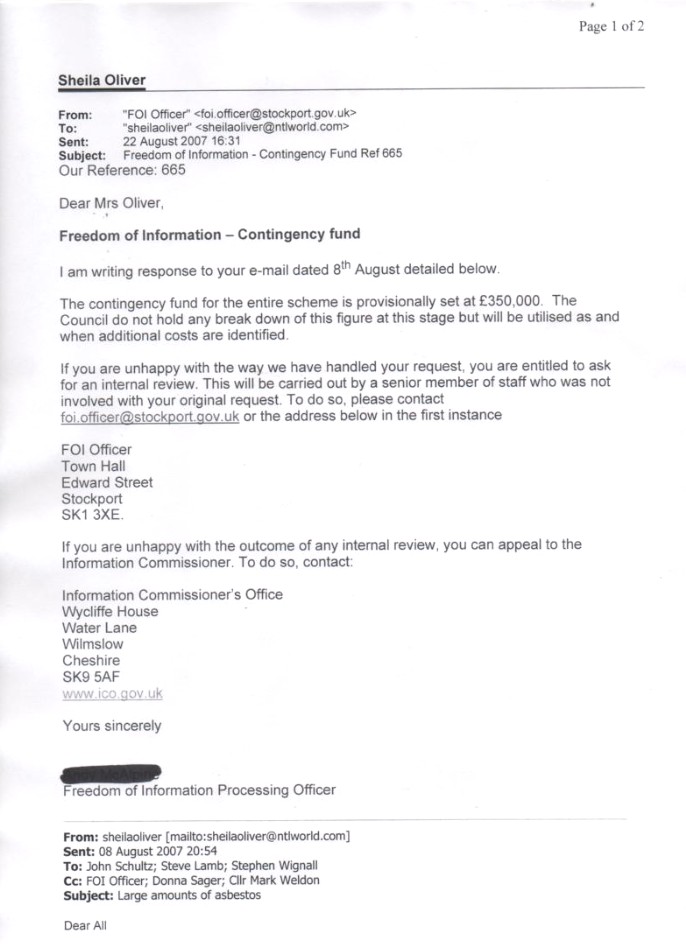

FoI response to request 618 sent on 8/8/2007

Response to FOI request received 09/08/2007

"Dear Mrs Oliver

I am writing in response to your e-

As you are aware the cost of the recommendations of Sport England is estimated to be £500,000."

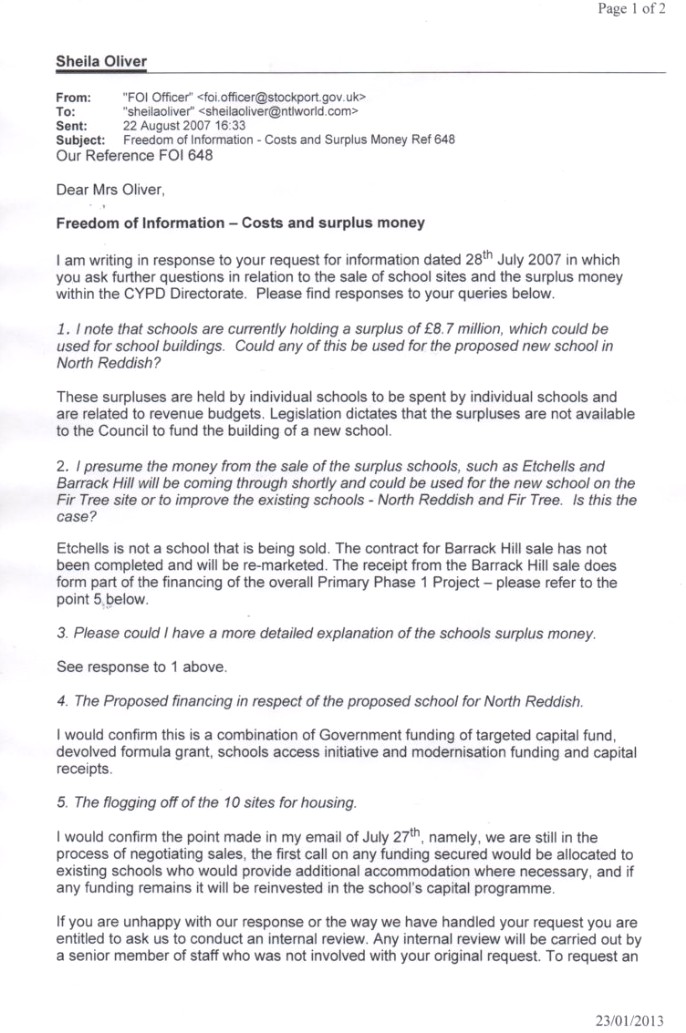

Our Reference: FOI 765

Dear Mrs Oliver,

Freedom of Information – Name of Insurance Company

I am writing in response to your request for information dated 10 th October detailed below.

The Council has various policies with various insurance companies but Zurich Municipal is the Council's building insurers.

The Council has not yet appointed a contractor for the sites and therefore does not hold this information.

If you are unhappy with our response or the way we have handled your request you are entitled to ask us to conduct an internal review. Any internal review will be carried out by a senior member of staff who was not involved with your original request. To request an internal review please email foi.officer@stockport.gov.uk in the first instance or write to:

FOI Officer

Town Hall

Edward Street

Stockport

SK1 3XE

If you are unhappy with the outcome of any internal review you can complain to the Information Commissioner. To do so please contact:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

www.ico.gov.uk

01625 545745

Yours sincerely,

XXXX

Freedom of Information & Data Protection Processing Officer

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: 08 October 2007 16:40

To: FOI Officer

Subject: Re: FOI 732 -

Dear XXXX,

Even I, thick as I definitely am, know you don't have to insure a school which isn't yet built.

What is the name of the insurance company the Council generally uses? I presume it just uses one or maybe I am wrong.

I will also need to contact the insurance company of the contractors, because their insurers will need to have sight of the evidence we have regarding contamination.

Kind regards

Sheila

-

Stockport Council

Anti-

Author: Corporate Governance Group Version: 1.3 Date 9th March 2009 Status: Approved

1. Introduction

1.1 As part of its vision to create an attractive and thriving Stockport, the Council is committed to safeguarding public funds and maintaining the highest standards of probity. In order to fulfil this commitment, it is crucial that the Council’s resources are properly safeguarded and the manner in which these resources are used is underpinned by a secure and controlled environment.

1.2 Stockport Council takes a zero-

1.3 This Anti-

The policy is underpinned by a Anti-

Scope

2.5 The policy applies to:

All Council employees (permanent and temporary, including employees working within schools)

Elected members

Agency workers

Consultants

2.6 In addition, the Council expects that all stakeholders should maintain the highest standards of integrity in their dealings with the Council. This means being honest and open in their own dealings with the Council and being proactive in reporting genuine suspicions of fraud, irregularity or improper conduct by other Council stakeholders (see above list). Stockport Council expects that employees of partner organisations working with the Council will have an awareness of the Council’s Anti-

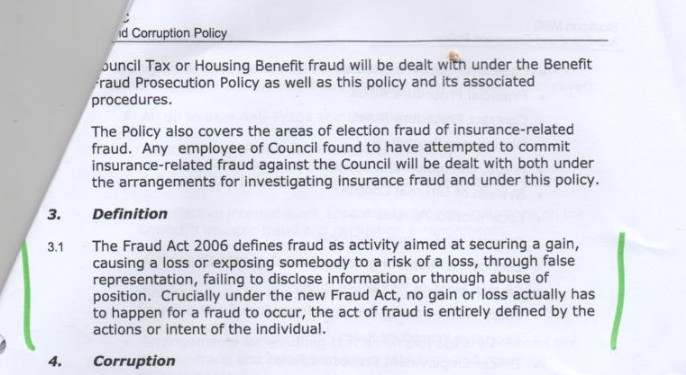

2.7 The Council also has in place a Benefit Fraud Prosecution Policy setting out how both Housing Benefit and Council Tax Benefit fraud will be dealt with. Any employee of Stockport Council suspected of committing

Council Tax or Housing Benefit fraud will be dealt with under the Benefit Fraud Prosecution Policy as well as this policy and its associated procedures.

The Policy also covers the areas of election fraud of insurance-

Definition

The Fraud Act 2006 defines fraud as activity aimed at securing a gain, causing a loss or exposing somebody to a risk of a loss, through false representation, failing to disclose information or through abuse of position. Crucially under the new Fraud Act, no gain or loss actually has to happen for a fraud to occur, the act of fraud is entirely defined by the actions or intent of the individual.

Corruption

4.1 Corruption may be defined as any conduct which amounts to:

The offering, giving or accepting of an inducement or reward or indication of possible future reward, which would influence the actions taken by the Council, its members or officers.

Dishonesty or breach of trust by a public officer in the course of his / her duty;

The use of undue influence such as bribery or blackmail, which includes the use of election fraud. Any person who directly accepts, agrees of offers to accept any gratification from any other person to benefit him / herself or any other person is guilty of the crime of corruption.

Hiring or promoting an individual inappropriately, or unduly influencing the hiring or promoting of an individual or otherwise inappropriately influencing the level of remuneration of an individual.

The person who makes the offer or inducement to another to commit a corrupt practice is also guilty of the crime of corruption. Although there is an active and a passive side to the crime, both parties are equally guilty of corruption.

Corporate Framework

5.1 This policy operates within the overall corporate framework designed to ensure appropriate standards of conduct from Council employees and other stakeholders. This Anti-

Council Constitution

Code of Conduct for Officers

Code of Conduct for Elected Members Financial Procedure Rules Contract Procedure Rules Disciplinary Procedure Fraud, corruption and irregularity procedures System of Internal Control Local procedure rules Scheme for Financing Schools Confidential Reporting Policy (Whistleblowing) Council Meeting Procedure Rules Policy Framework and Budget Procedure Rules Executive Procedure Rules Officer Employment Procedure Rules

6. Mechanism for Reporting Suspicions of Fraud or Corruption

6.1 Staff should report suspicions through their line manager or direct to the Chief Internal Auditor or Group Auditor. Where line managers receive allegations of fraud from staff, these should be reported to the Chief Internal Auditor.

6.2 The Council also has in place avenues for staff to report suspicions of fraud and corruption through the Confidential Reporting Policy. Matters will be dealt with where possible in confidence and in accordance with the Public Interest Disclosure Act 1998. This statute protects the legitimate personal interests of staff.

All referrals of suspected fraud, corruption or other irregularity will be referred to the Chief Internal Auditor for determination of the appropriate course of action.

Roles and Responsibilities

7.1 This section sets out the roles and responsibilities of groups and individuals within the Council to contribute to the effective management of fraud risk.

Corporate Director, Business Services (Section 151 Officer)

7.2 The Corporate Director, Business Services in his role as the Council’s Section 151 Officer has overall responsibility for establishing and maintaining a sound system of internal control. This system of internal control is designed to respond to and manage the whole range of risks that the Council faces. Managing fraud risk will be seen in the context of the management of this overall range of risks.

Corporate Governance Group

7.3 The Corporate Governance Group has responsibility for ensuring the Council has adequate counter-

Arrangements for ensuring that all employees are aware of the counter-

Fraud and Irregularities Panel

7.4 The Council has established a Fraud and Irregularities Panel to take responsibility for ensuring that suspected frauds or irregularities are appropriately investigated and that the appropriate action is taken following the outcome of the investigation.

7.5 The Fraud and Irregularities Panel is responsible for: Ensuring that a prompt and comprehensive investigation occurs in response to a suspected fraud or irregularity referral Ensuring that appropriate legal or disciplinary action is taken against perpetrators of fraud Ensuring that action is taken to recover Council assets where possible Managing the dissemination of information about frauds to third parties Ensuring that the weaknesses in procedures that allowed the fraud to occur are identified Ensuring that appropriate action is taken to minimise the risk of

similar incidents in the future Council Employees

7.6 Every member of employees is responsible for;

Acting with propriety in the use of Council resources and the handling and use of public funds.

Conducting themselves in accordance with the seven principles of public life set out in the first report of the Nolan Committee ‘Standards in Public Life’. These are; selflessness, integrity, objectivity, accountability, openness, honesty and leadership.

Being alert to the possibility that unusual events or transactions could be indicators of fraud.

Reporting details immediately through the appropriate channel if they suspect that a fraud has been committed or see any suspicious acts or events.

Cooperating fully with the investigating officer where a fraud investigation is taking place.

7.7 Council employees are often a key element in the prevention and detection of fraud and the standards expected of Council employees are set out in the Code of Conduct for Officers. In addition, employees in certain professions will also be expected to abide by codes of conduct and / or ethics set out by their professional institutes eg Accountants, Architects, Engineers etc.

7.8 Fraud prevention, detection and reporting is the responsibility of all officers and members of the Council and this policy requires that all suspicions of fraud are reported to the Chief Internal Auditor. Reports may also be made under the Council’s Confidential Reporting (Whistleblowing) Policy to one of the named officers within the policy, however where a suspicion of fraud is reported, this should be referred to the Chief Internal Auditor for determination of the appropriate responsibilities for investigation.

7.9 Where an investigation concludes that there has been a breach of the Code of Conduct for Officers, disciplinary action may be taken under the Council’s Disciplinary Procedure.

7.10 Where criminal activity is found to have taken place, the matter may be referred to the police in accordance with the Council’s Fraud Response Procedures. The Council will also carry out its own investigation in order to determine whether disciplinary action is appropriate. Disciplinary action may be taken independently of any police decision to prosecute. The Council’s policy is to take recovery action to recoup any losses sustained through fraudulent acts by employees or other stakeholders.

Elected Members

7.11 The standards required of Elected Members are set out in:

The National Code of Local Government Conduct Local Government Act 1972 Local Authorities’ Members Interest Regulations 1992 The Council’s Constitution

7.12 Elected Members are required to comply with this policy and where suspicions of fraud are raised, these should be reported appropriately. Where there are concerns regarding the conduct of elected members, these should be reported to the Council’s Monitoring Officer or Deputy Monitoring Officer.

Audit Committee

7.13 The Audit Committee has responsibility for considering the effectiveness of the authority’s risk management arrangements, control environment and associated anti-

Standards Committee

7.14 The Standards Committee is responsible for promoting and maintaining high standards of conduct by Councillors and co-

Senior Management

7.15 The Council’s senior management are responsible for:

Ensuring an adequate system of internal control operates within their area of responsibility.

Creating and maintaining an effective anti-

Ensuring employees feel able to raise suspicions of fraud or irregularity in an environment of trust.

Ensuring awareness of the Council’s counter-

Ensuring their employees are adequately trained to operate within the Council’s policy framework.

Ensuring their employees are appropriately trained to fulfil their responsibilities for reporting suspicious activities.

7.16 Where an investigation concludes that fraud or other irregularities have taken place, a report of the findings of the investigation will be presented in line with the Fraud Response Plan to the corporate Fraud Response Group. This group will determine the appropriate course of action. It is the responsibility of senior management to implement this action and lead any disciplinary or legal action.

Operational Management

7.17 Operational managers are responsible for implementing and maintaining an adequate system of internal control within their areas. This includes responsibility for the prevention and detection of fraud. Management’s responsibility for maintaining adequate controls also includes the monitoring and reviewing of systems to ensure that controls are operating effectively. In addition, where frauds have occurred, management are responsible for implementing any additional controls to minimise the risk of future incidents.

7.18 Management are also responsible for training and development of employees to ensure they are aware of the Council’s policies and procedures and that they agree to operate within these parameters.

7.19 In addition, management are responsible for reporting concerns raised by their employees to the Chief Internal Auditor.

Internal Audit

7.20 Internal Audit is responsible for providing assurance that the Council has adequate and effective anti-

Where suspected fraud is referred to the Chief Internal Auditor, an initial assessment of the information available will be carried out and where appropriate the Fraud and Irregularities Response Procedure will be invoked.

Summary

8.1 This policy has set out the Council’s position on fraud and established the roles and responsibilities of Council stakeholders in contributing to creating a robust anti-

Level 2 – Condensed Text

to be published on Participant’s website

Stockport Council is required by law to protect the public funds it administers. It may share information provided to it with other bodies responsible for auditing or administering public funds to prevent and detect fraud. The Audit Commission audits the accounts of Stockport Council and is also responsible for carrying out data matching exercises.

Data matching involves comparing computer records held by one body against other computer records held by either the same or another body to see how far they match. These records usually contain personal information. Computerised data matching allows potentially fraudulent claims and payments to be identified. Where a match is found, it indicates that there is an inconsistency which requires further investigation. No assumption can be made about whether an inconsistency is due to fraud, error or another explanation until an investigation is carried out.

The Audit Commission currently requires Stockport Council to participate in a data matching exercise to assist in the prevention and detection of fraud. The Council is required to provide particular sets of data to the Audit Commission for matching for each separate exercise. These are set out in the Audit Commission’s guidance which can be found at www.audit-

Part 2A of the Audit Commission Act 1998 gives the Audit Commission the statutory power to request and use data in data matching exercises. This means that under the Data Protection Act 1998, neither Stockport Council nor the Audit Commission needs to obtain the consent of individuals involved to use their personal information in this way.

Data matching carried out by the Audit Commission is subject to a Code of Practice. This can be found at www.audit-

For further information about the Audit Commission’s legal powers and the reasons why it matches particular information, please see www.auditcommission.

gov.uk/nfi/fptext.asp. For further information about data matching at Stockport Council please contact the Data Protection Officer using the information under related contacts.

-

From: Sheila Oliver <sheilaoliver@ntlworld.com>

Subject: Fraud Act 2006

To: "Anwar Majothi" <anwar.majothi@stockport.gov.uk>

Cc: "bailey.harding" <bailey.harding@ntlworld.com>, "Syd Lloyd" <syd@sparkling-

Date: Monday, 31 August, 2009, 8:01 AM

Dear Mr Majothi

From the Fraud Act 2006:-

Fraud

1 Fraud

(1) A person is guilty of fraud if he is in breach of any of the sections listed in subsection (2) (which provide for different ways of committing the offence).

(2) The sections are—

(a) section 2 (fraud by false representation),

(b) section 3 (fraud by failing to disclose information), and

(c) section 4 (fraud by abuse of position).

(3) A person who is guilty of fraud is liable—

(a) on summary conviction, to imprisonment for a term not exceeding 12 months or to a fine not exceeding the statutory maximum (or to both);

(b) on conviction on indictment, to imprisonment for a term not exceeding 10 years or to a fine (or to both).

(4) Subsection (3)(a) applies in relation to Northern Ireland as if the reference to 12 months were a reference to 6 months.

2 Fraud by false representation

(1) A person is in breach of this section if he—

(a) dishonestly makes a false representation, and

(b) intends, by making the representation—

(i) to make a gain for himself or another, or

(ii) to cause loss to another or to expose another to a risk of loss.

(2) A representation is false if—

(a) it is untrue or misleading, and

(b) the person making it knows that it is, or might be, untrue or misleading.

(3) “Representation” means any representation as to fact or law, including a representation as to the state of mind of—

(a) the person making the representation, or

(b) any other person.

(4) A representation may be express or implied.

(5) For the purposes of this section a representation may be regarded as made if it (or anything implying it) is submitted in any form to any system or device designed to receive, convey or respond to communications (with or without human intervention).

3 Fraud by failing to disclose information

A person is in breach of this section if he—

(a) dishonestly fails to disclose to another person information which he is under a legal duty to disclose, and

(b) intends, by failing to disclose the information—

(i) to make a gain for himself or another, or

(ii) to cause loss to another or to expose another to a risk of loss.

4 Fraud by abuse of position

(1) A person is in breach of this section if he—

(a) occupies a position in which he is expected to safeguard, or not to act against, the financial interests of another person,

(b) dishonestly abuses that position, and

(c) intends, by means of the abuse of that position—

(i) to make a gain for himself or another, or

(ii) to cause loss to another or to expose another to a risk of loss.

(2) A person may be regarded as having abused his position even though his conduct consisted of an omission rather than an act.

I think what has gone on over Harcourt Street and possibly over Mr Parnell, who suffered a financial loss, is covered above.

I look forward to your comments.

Yours

Mrs Sheila Oliver

Stockport's Freedom of Information Campaigner

Dear Mrs Oliver,

I am writing in response to your request for information (ref FOI 6704).

The relevant Council Service(s) has searched for the requested information and our response is as follows.

1) Why have I paid BAM £60,361.02 for construction work in October 2012 when the school has been opened well over a year?

The payment is part of the ongoing process of settling the contract final account. This interim payment of £60,361.02 includes the valuation of the following items:

1. Additional works to reception area

2. External works delayed/postponed due to weather/time of year

3. Firming up final costs within the account

2) Why have I bought 100 people breakfast when jobs are being lost and services cut?

Further to your recent information request about the provision of a breakfast buffet for 100 people I have pleasure in sending you more comprehensive details about the purchase. The breakfast in question took place at Stockport Council’s Annual Developers Event on 10th October 2012.

The Developers Event is high profile event that enables Stockport Council to showcase the opportunities that exist locally for development and investment across the borough. It attracted 100 property developers and agents, providing an excellent opportunity for the Council to engage with the development sector about the Council’s progress in bringing forward town centre development projects that will bring benefit to both the residential and business community. Feedback from the event highlighted that attendees found the event highly beneficial, and that it has significantly raised the profile of the development opportunities that exist in Stockport Town Centre.

The Developers Event was hosted at a Grade A commercial property that is currently vacant within Stockport. The use of a vacant unit meant that we were able to secure a venue for no cost, however no onsite catering was available and a light breakfast was bought in for attendees, given the fact the event began at 7:30am. Quotations for the catering were requested from local companies who have experience working at high profile events of this nature, and the services of Door 2 Door Brassiere were secured as a result of this. This was the first time that the Economic Development and Regeneration programmes section of the Council had worked with Door 2 Door Brassiere however the quality of catering they provided, equipment supplied and service offered was considered to be excellent value for money.

3) What SEMMMS work has NPS done for that huge sum of money? NPS is so incompetent I am quite heartened to see they are involved

NPS (Stockport and Norwich offices) have provided professional advice on land and property related matters including acquisition and compensation along the proposed scheme route. This has also involved liaison with landowners affected by the scheme proposals and local residents.

4) What were these architects' fees for:-

160,587.70

NPS STOCKPORT LTD

ARCHITECT FEES AUGUST 2012

These fees relate to various professional services undertaken relating to the month of August for 125 different projects across the S.M.B.C. portfolios.

These Services include;

Architectural

Building Surveying

Quantity Surveying

M&E Services

Facilities Management

Estates and Asset Management

If you are unhappy with the way we have handled your request for information, you are entitled to ask for an internal review; however you must do so within 40 working days of the date of this response. Any internal review will be carried out by a senior member of staff who was not involved with your original request. To ask for an internal review, contact foi.officer@stockport.gov.uk in the first instance.

If you are unhappy with the outcome of any internal review, you are entitled to complain to the Information Commissioner. To do so, contact:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

www.ico.gov.uk

01625 545 745

Yours sincerely,

Simon Oldfield

Freedom of Information/ Data Protection Officer & RIPA Coordinator

Stockport Council

Town Hall

Stockport

SK1 3XE

Tel: 0161 474 4048

Fax: 0161 474 4006

http://www.stockport.gov.uk

Tel: 0161 474 4048

Fax: 0161 474 4006

http://www.stockport.gov.uk

Need further information? See our Information Management FAQs

Confidentiality: This email, its contents and any attachments are intended only for the above named. As the email may contain confidential or legally privileged information, if you are not, or suspect that you are not, the above named or the person responsible for delivery of the message to the above named, please delete or destroy the email and any attachments immediately and inform the sender of the error.

If it is Council owned land the Statement of Accounts is quite clear. The Council are in the Catch 22. They might say 'oh it's worth nothing on it's present use so we didn't value it" BUT if they say that it most certainly is worth something on it's change of use to a school. That would be quite a revelation. Where is that money coming from. That might ( I'm jumping several steps) explain one reason why the cost is so high.

-

I am surprised the Council does not hold a current valuation of the Harcourt St recreational land.

In the Councils' Statement of Accounts for 2006 to 2007 on page 18 it clearly states under Statement of Accounting Practices "land, operational properties and other operational assts are included in the Balance Sheet at the lower end of net current replacement cost or net realisable value in existing use." That suggests Land is valued into the Balance Sheet.

On the Balance Sheet itself page 25 there is a mention of "Other Land and Buildings" at £342.5m. Thus the above suggestion is confirmed by the Balance Sheet valuation which includes Land.

On page 41 there is a breakdown of the type of assets which comprise and come under the definition of "Other Land and Buildings". I would have thought it inevitable that the land at Harcourt St would come under one of these huge number of catch all assets and therefore have a value attached.

-

Separately I have been told that the Council land at Fir Street Site itself has a value for it's anticipated sale.

Therefore as Harcourt Street is Council Land and that would be reported in the Councils Balance Sheet either in the catch all Other Land and Buildings or some similar category. All this evidence is contrary to their answer that you do not hold a valuation of the land. If they do not that would seem to be in contravention of the Councils' established Accounting Practices.

Regarding my question regarding the transfer process to Childrens and Young Person's Deepartment I refer to the Statement of Accounts 2006 to 2007 page 42 "Movement of Tangible Fixed Assets". On this Schedule 20 there is a sub-

Obviously the net affect to the Balance Sheet of transferring the value of Harcourt St to CYPD should be zero. However my question remains; what is the process and associated figures. I am particularly interested if any change will be made to the Book Value.

-

This does sound very odd. I can sort of just accept that there are odd small pockets of land that have been in the community from sort of medieval times and their status as perhaps a grazing ground for horses has never nor never will change.

I understand that for some considerable time it has been earmarked as the site of a new school for which capital budgets have been drawn up. Surely surely someone must have thought what is the value of this land. Are they saying the land will be zero valued for this project.

There are transfers and indeed has to be a transfer from one Asset register to another which is not what I was told. If there a is no value for the Harcourt St land in the School price that makes the £8.5m even more expensive than a "normal" new build school.

The point is, I think, why is this school costing so much money? Or is the point this is costing so much money because you are having to spend so much on contamination and SMBCwon't admit it. or is the point you lot have just lost the plot and does anyone understand why this school is costing so much.

-

The whole case against building a School at Harcourt street is that it is to be built on a past tip with the available scientific information that this could prove a serious hazard to health. This scientific information is being "covered up" or is not being presented truthfully. Indirect evidence of this is that the budgeted cost of the school is rising exponentially and it is supposed/alleged that this extra cost is to cover the possible undeclared site decontamination costs After approval has been given but before the school has been built.

-

To: sheilaoliver

Cc: Donna Sager ; Louise Grainger

Sent: Tuesday, November 06, 2007 11:30 AM

Subject: FOI 761 -

Dear Mrs Oliver

Freedom of Information -

I am writing in response to your request for information detailed below.

1. There are two types of funding for Education Services, revenue funding and capital funding.

Revenue Funding

The “Education Services” category in the Statement of Accounts (Consolidated Revenue Account) comprises revenue expenditure and income in relation to nursery, primary and secondary schools as well as non school funding. The latter comprises strategic management of non-

For 2006/07, the arrangements for Government support for the revenue funding of schools changed. Previously funds were provided as part of the Council’s overall Revenue Support Grant and National Non-

The Council’s revenue expenditure on schools is primarily funded by this Dedicated Schools Grant (DSG). DSG is ring-

Revenue funding is also provided by “devolved grants”. These are grants specifically allocated to each type of school, comprising amongst others the Standards Fund Grant, including any matched LA funding, and the Schools Standards Grant. In 2006/07 there is also a general element within the Revenue Support Grant which now forms part of the “Children’s Services” element of the annual settlement. This funds the non school services noted above.

Capital Expenditure generally represents money spent by the Council on purchasing, upgrading and improving schools. Capital spend and funding is reflected in the fixed assets, capital financing and capital grants and contributions notes to the Statement of Accounts. It is not normally possible to specifically identify the Education elements from these notes.

2. The expenditure of £221.6m in the 2005/06 Statement of Accounts is as described in point 1. The income of £59.4m includes devolved grants but does not include the main funding for Education Services which formed part of the “Revenue Support Grant” and “Distribution from Non – Domestic Rate Pool” figures of £199m. This funding in 2005/06 was calculated via the Schools Formula Spending Shares.

In 2006/07, £141m has been included in income in the “Education Services” section of Net Cost of Services in the Income and Expenditure Account (which replaced the Consolidated Revenue Account in 2006/07) for the DSG.

3. The Council spent £14.3m on its Education capital programme in 2006/07. Of this £8.1m was funded by government grants.

The main element of government grants is “Devolved Formula Capital” (DFC), which amounted to £4.1m in 2006/07.

Other capital grants comprise Sure Start, Standards Fund and Modernisation grants.

4. The DSG funding is driven by the number of pupils that the Local Authority provides or commissions education for from 3 years old to 16 years old. Each pupil attracts a flat rate per pupil of £3,706.45 (£3,484.44 in 2006/07) and in 2007/08 the grant will amount to £146 million.

Other specific grants such as the Standards Fund, School Standards Grant, Sure Start grants etc are based on a combination of factors such as pupil numbers, bids made by the Council, deprivation statistics, ministerial priorities etc.

The non school funding part of RSG is based upon population, income support data and ethnicity.

DFC is an amount allocated each year to primary and secondary schools to be spent by them on their priorities in respect of buildings, ICT and other capital need. Allocations of DFC are based on pupil numbers.

More information on the DSG can be found at the following website:

http://www.teachernet.gov.uk/management/schoolfunding/2006-

More details on DFC can be found at the following website: http://www.teachernet.gov.uk/management/resourcesfinanceandbuilding/FSP/nds/

The 2006/07 Statement of Accounts can be accessed using the following link: www.stockport.gov.uk/statementofaccounts

If you are unhappy with our response or the way we have handled your request you are entitled to ask us to conduct an internal review. Any internal review will be carried out by a senior member of staff who was not involved with your original request. To request an internal review please emailfoi.officer@stockport.gov.uk in the first instance or write to:

FOI Officer

Town Hall

Edward Street

Stockport

SK1 3XE

If you are unhappy with the outcome of any internal review you can complain to the Information Commissioner. To do so please contact:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

www.ico.gov.uk

01625 545745

Yours sincerely,

XXXX

Freedom of Information & Data Protection Processing Officer

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: 06 October 2007 08:18

To: Louise Grainger

Subject: Education

Dear Ms Grainger

I would be grateful if you could help point me in the right direction on a number of issues regarding Education in the Statement of Accounts. I am trying to understand how much money is supplied in grants from the government to the Education budget. I realise this is complicated but perhaps the following questions will get me started.

1 I would assume there are 2 main sorts of grants; one for the Operational Costs and one for the Capital Investment of new schools and infrastructure. Assuming your confirmation that that is true then as a rule would the grants for Replacement and Refurbishment of

existing Schools normally come under Operational Costs. I can appreciate it could be confused if an existing school is increased in size and the grant is divided between the existing size and the extension costs but can we ignore that possibility in your answer.

2 When I read the Statement of Accounts for 2005 to 6 can I assume the Gross Expenditure of £221.6m includes all grants excluding Capital grants for New Projects and that the Government Grant is £59.4m leaving Net Expenditure of £162.2m to be allocated from private and business Council Tax. If I am wrong where in the Accounts can I find the Government Grant towards the Operating Costs for that year.

3 Similarly where can I find the Total Government Capital Grant to be be used for new Education Projects.

4 I would assume it is a huge and vastly complicated issue but what are the main parameters that Government Operational Grants are given. Is it the Borough population; the amount allocated from Council Tax,

the school population, the adherence to Government issues say of number of under privileged children or achievement of pass rates at various ages.

I know this latter could be a huge subject but an answer in very general terms with perhaps a reference or two to Government websites would suffice

Kind regards

Sheila Oliver

**********************************************************************

This email, and any files transmitted with it, is confidential and

intended solely for the use of the individual or entity to whom they

are addressed. As a public body, the Council may be required to disclose this email, or any response to it, under the Freedom of Information Act 2000, unless the information in it is covered by one of the exemptions in the Act.

If you receive this email in error please notify Stockport e-

Thank you.

I asked the question because Councillor Weldon said Stockport had had their

grant reduced by Government. I didn't ask that question but asked

what do Government give in the line of grants for Education. Louise

has given the answer and it's enormous and if they have reduced an

amount anywhere it's probably either because the number of pupils has

reduced or there is no proof of need for various kinds of Special

Grants.

There are a large number of grants with different names and

objectives. Probably a result of different initiatives by different

governments.

Revenue Expenditure is the money spent just to keep the schools going

day to day (mainly) and last year was £221.6m. Stockport got Devolved

Grants of £59.4m from the government. These DGs are specific grants

depending on the type of School Nursery, Primary, and Secondary. On

top of that are Dedicated School Grant of £141m thus totalling £200.4m

from Government leaving SMBC to find £21m !!!!!

Louise is not very clear but the method of funding was

changed in 2006/7. I THINK repeat think what she is saying is that in

the previous year the grant was called Revenue Support Grant and

Distribution from Non Domestic Rate Pool and amounted to £199m ( more

than £141m) BUT did not include £59.4m

I'm saying 2005/6 £199m from Government 2006/7 only

£141m from Government but £59.4 m from another grant

more than makes the difference.

I don't think Weldon is actually lying; it looks like the Gov may have reduced one

grant; quite True Weldon but you've forgotten to tell your readers the

Gov have more than made up with another!

-

On the capital side SMBC spent £14.3m in 2006/7 of which £8.1m was

paid for by Government 56.6%

-

In 2005/6 the Education the Revenue Expenditure was £221.6m; income £59.4m Net Expenditure of £162.2m but that disguises the fact that further grants were made available to total £199m. Thus actually leaving SMBC to fund £221.6 -

In 2006/7 the grant was supplied in a different manner with different titles that my mind cannot get around.

Essentially though the Gross Expenditure was £224.1m; the Total grants and I realise some money might be from reserves from previous years and all such provisos but never the less the Total grants for 2006/7 was £212.2m leaving SMBC to fund £11.9m.

It is my understanding mostly correct and in general terms can I make the Statement that in 2006/7 SMBC, that is me and you as ratepayers spent less money on Education because the government paid more compared to 2005/6.

-

What exactly is "refund of liquidated damages deducted for Vale View School Project"?

‘Under the building contract, the employer is entitled to deduct liquidated damages in the amount specified in the contract documents from payments due to the contractor. This sum is expressed as £/per calendar week or pro rata thereto and is deducted where the contractor fails to complete the works by the contract completion date or any extended date that may be awarded under the contract. Vale View had a damages figure of £16,800 per calendar week and at the point of deduction the contract had overrun the completion date by 2 weeks and 2 days. Requests by the contractor for extensions of time to the completion date are allowed under the terms of the contract which are then considered by the Employers Agent. A request for an extension of time was received following the deduction of damages which was subsequently approved by the Employers Agent for the full period of 2 weeks and 2 days. The result of this extension to the original completion date was to reimburse the contractor the amount of damages previously deducted being the sum of £38,400.’

Schools Capital Enquiry Team

Department for Education and Skills

Mowden Hall

Staindrop Road

Darlington

Co. Durham

DL3 9BG

E-

Phone: 01325 391716

Thank you for your email of 17 August, requesting information on the cost of building a primary school.

You may wish to know that this Department provides information on school building costs / funding levels at www.teachernet.gov.uk/costinformation. You may also wish to refer to the funding guidance for the Building Schools for the Future programme, at http://www.p4s.org.uk/guidance.htm.

Furthermore, there are other sources of published cost information, such as the subscription Building Cost Information Service of the Royal Institution of Chartered Surveyors.

Finally, promoters of school projects should seek professional advice on the costs of their projects.

Yours sincerely

Joanna Seaman

Public Communications Unit

Your correspondence has been allocated the reference number 2007/0056016. To correspond by email with the Department for Children, Schools and Families please contact info@dcsf.gsi.gov.uk.

If you have any further queries why not browse our Popular Questions website. This site has been built to allow you to quickly find the answer to your question http://www.dcsf.gov.uk/popularquestions

The original of this email was scanned for viruses by the Government Secure Intranet Anti-

Communications via the GSi may be automatically logged, monitored and/or recorded for legal purposes.

-

If you look at this site it gives the cost per pupil for a primary school as £10372 so a 600 pupil school would cost approx £6.25m so your original estimate of £5.4m is cheapish. Without a doubt the current estimate of £8.5m is 36% or one third above the Official Average given by this very official Government body. There has to be a reason and is a very valid question. In the private sector new houses, factories etc etc don't deviate much from the average, so why should a school.

The query is obviously -

This Department provides information on school building costs / funding levels at www.teachernet.gov.uk/costinformation. You may also wish to refer to the funding guidance for the Building Schools for the Future programme, at http://www.p4s.org.uk/guidance.htm.

£10,372 is for 2006/7 and the school was to be started in 3 years, so the cost will

increase by Inflation of say 4.5%. So 2007/8 cost is £10,839 or £6.5m.

Re reading the site it seems land and equipment is not included. But

there is a separate section that gives equipment costs.

Also there is a section that gives geographical factors Stockport is

0.94 so £6.25m becomes £5.88m which is now nearer the original figure.

From the site www.teachernet.gov.uk/cost information

Cost Multipliers are costs per pupil for the construction of accommodation to provide for additional pupil places.

The 2006-

Primary £ 10,372

Secondary £ 15,848

Post 16 £ 17,013

Therefore for a 525 pupil Primary School the cost of construction of accommodation for additional places is £10372*525=£5.445m. Stockport has a variance of 0.94 to allow for regional cost differences therefore a Budget Cost of £5.25m appears reasonable to put up on an aquired site.

There has to be some transfer.

I imagine the land is on the Asset Register of Parks and Recreation ( a list of all the things that department has to care for and maintain). But in the future Schools will use the land for its own purpose of building a school on it and the use of the land for recreation will cease. It is now not only unfair for recreation to keep the land on its register but the responsibility has to lie where the use is. Therefore it has to be transferred to the Asset Register of Schools. No money changes hands but within SMBC, Schools has effectively "bought" the land from Parks and Recreation and is now responsible for the care and maintenance of the land.

Assuming I am right ( I am)

92 Primary Schools have an average 170 pupils at an average value of £0.98m. A 600 pupil School would have a hypothetical net book value of £3.44m.

The ratios from the other Gov source gave a new build cost for a 600 pupil School of £10372*600*0.94 = £5.85m. Conclusion A 600 pupil Primary School is MUCH bigger than the average.

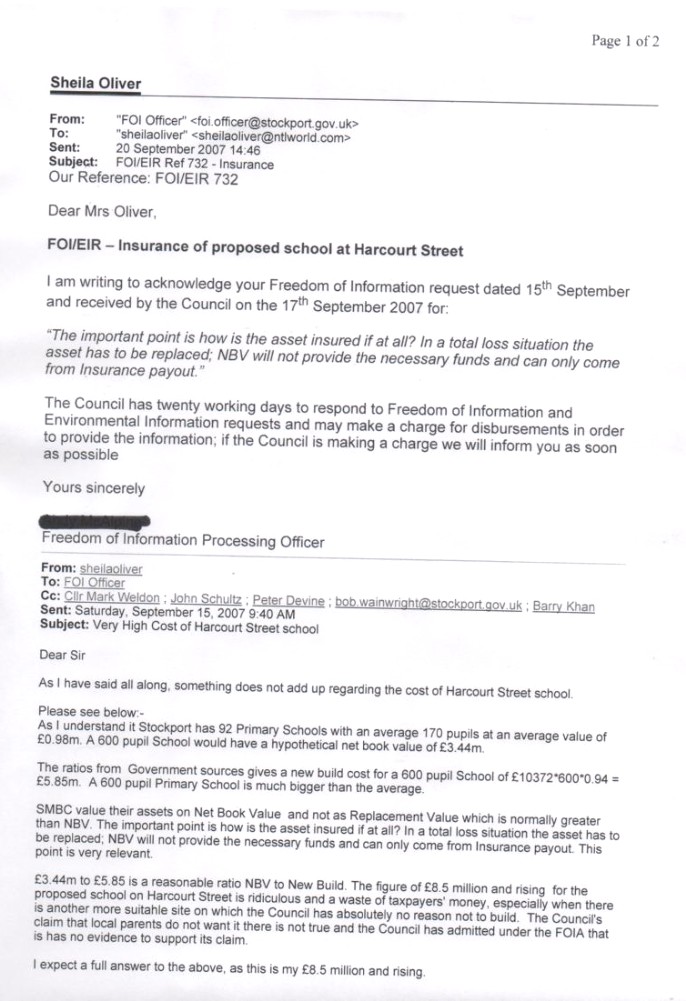

SMBC value their assets on Net Book Value not as Replacement Value which is normally greater than NBV. The important point is how is the asset insured if at all. In a total loss situation the asset has to be replaced; NBV will not provide the necessary funds and can only come from Insurance payout. The point may be irrelevant to me but I assure you is of deep significance on the risks taken by residents.

£3.44m to £5.85 is a reasonable ratio NBV to New Build. With the £8+ million figure something is wrong.

Email received 19/02/2008 at 12.37

Mrs Oliver,

I stated that I assumed that you had mistaken the estimated simple build cost of a school building with the total project cost. On closer inspection of the figures from yourself my assumption has proven to be correct.

Yours M.E Weldon

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: Mon 18/02/2008 21:18

To: FOI Officer

Cc: Cllr Mark Weldon; John Schultz

Subject: Executive Meeting

Dear FOI Officer

In response to a public question at tonight's executive meeting Cllr Weldon agreed that there were costs over and above the £5,400,000 stated building cost for the Harcourt Street School known to the Council as early as December 2005 -

So, please may I see the documentary evidence of the financial workings out that the Harcourt Street site was financially a better option than the Fir Tree site. This should be interesting.

Kind regards

Sheila

-

Email received 10/03/2008 at 14.20

Mrs Oliver,

I merely announced the ruling of the school adjudicator who was extremely sympathetic to the unexpected delays the project had encountered. We had to get the formal agreement of the adjudicator before any final formal decision is taken by the executive.

Regards,

Mark Weldon

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: Fri 07/03/2008 17:29

To: FOI Officer; John Schultz

Cc: Cllr Paul Carter; Cllr Mark Weldon; Cllr Dave Goddard

Subject: Re: Risk register -

Dear Ms Naven

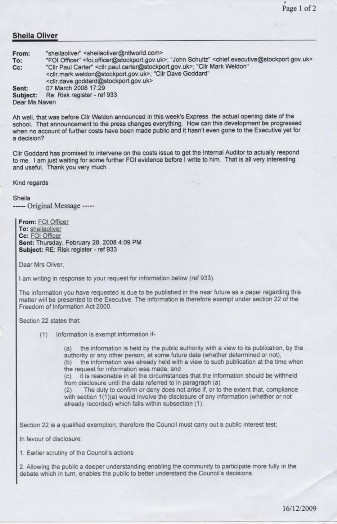

Ah well, that was before Cllr Weldon announced in this week's Express the actual opening date of the school. That announcement to the press changes everything. How can this development be progressed when no account of further costs have been made public and it hasn't even gone to the Executive yet for a decision?

Cllr Goddard has promised to intervene on the costs issue to get the Internal Auditor to actually respond to me. I am just waiting for some further FOI evidence before I write to him. That is all very interesting and useful. Thank you very much .

Kind regards

Sheila

-

To: sheilaoliver

Cc: FOI Officer

Sent: Thursday, February 28, 2008 4:09 PM

Subject: RE: Risk register -

I am writing in response to your request for information below (ref 933).

The information you have requested is due to be published in the near future as a paper regarding this matter will be presented to the Executive. The information is therefore exempt under section 22 of the Freedom of Information Act 2000.

Section 22 states that:

(1) Information is exempt information if-

(a) the information is held by the public authority with a view to its publication, by the authority or any other person, at some future date (whether determined or not),

(b) the information was already held with a view to such publication at the time when the request for information was made, and

(c) it is reasonable in all the circumstances that the information should be withheld from disclosure until the date referred to in paragraph (a).

(2) The duty to confirm or deny does not arise if, or to the extent that, compliance with section 1(1)(a) would involve the disclosure of any information (whether or not already recorded) which falls within subsection (1).

Section 22 is a qualified exemption; therefore the Council must carry out a public interest test:

In favour of disclosure:

1. Earlier scrutiny of the Council’s actions

2. Allowing the public a deeper understanding enabling the community to participate more fully in the debate which in turn, enables the public to better understand the Council’s decisions.

In favour of withholding:

1. Information will shortly be in the public domain through a tried and trusted disclosure route.

2. Public and members will have opportunities to comment and influence decision making

The Council has decided that the public interest lies in withholding the information in this case.

If you are unhappy with the way we have handled your request you are entitled to ask for an internal review. Any internal review will be carried out by a senior member of staff who was not involved with your original request. To ask for an internal review, contact foi.officer@stockport.gov.uk in the first instance.

If you are unhappy with the outcome of any internal review, you are entitled to complain to the Information Commissioner. To do so, contact:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

www.ico.gov.uk

01625 545 745

Yours sincerely,

Claire Naven

Claire Naven

Data Protection & Freedom of Information Officer

Stockport Metropolitan Borough Council

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: 31 January 2008 07:32

To: FOI Officer

Cc: Cllr Paul Carter; f-

Subject: Risk register

Dear Sir

I note from the Harcourt Street risk register, which again I had to fight really hard for was it three months to see, that the Council considers the risk of requiring drainage works in excess of the allowed prov sum as high and also the risk of the Environment Agency requiring additions surveys with implications on delays or costs is also high. Given that, I would like to see any documents anywhere in the Council where any account has been taken of these potentially huge costs on this already massively rising cost of this school. The risk register was written in November and the planning application was rushed through in January. I presume in the interim someone took some sort of account of these potential costs -

Kind regards

Sheila

Mrs Oliver,

I rebut your allegations that there are "missing millions". The delays and modifications and additions to the project explain the increased estimated costs.

I rebut that there is any evidence of corruption. If there was I would immediately take it to the chief executive.

I rebut the allegation that I or any member of the executive does not exercise proper political oversight of council activities.

You are of course welcome to go to the district auditor.

I think that's clear, and polite.

Mark Weldon

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: Tue 11/03/2008 21:53

To: Cllr Mark Weldon

Subject: Re: CPOs Harcourt Street

God, this is confusing. What comments would you rebut? That I will go to the District Auditor regarding the missing millions, that some senior council officers are corrupt (watch this space) that you apply no checks and balances to them? Elucidate please.

I merely said because you wouldn't meet me (which you wouldn't at the time I wrote it) that you had your head in the sand on this issue of children's safety and when you did that you showed the counciltaxpayer that part of your anatomy. Quite mild really. Most of my letters have to pass the lawyers.

KR

Tired Old Trout

-

To: sheilaoliver

Sent: Tuesday, March 11, 2008 9:44 PM

Subject: RE: CPOs Harcourt Street

I would of course rebut your comments. What comments re my bottom ??

Mark W

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: Tue 11/03/2008 20:55

To: Cllr Mark Weldon

Subject: Re: CPOs Harcourt Street

Dear Councillor Weldon

Ah, but the issues where I am trying to establish exactly what has gone on

are in your area of responsibility. For example, it wasn't true that the

best financial solution was Harcourt Street above the Fir Tree site -

never, ever was and it certainly isn't true now. And there is no evidence

whatsoever that anyone wanted the school on the Harcourt Site. Not a

sausage and hundreds of letters against. We have to ask ourselves what has

gone on here. Is it corruption? We have to proceed next via the District

Auditor in examining this entire financial issue, once I get the facts from

Stockport Council, which is extremely difficult. This again ultimately and

quite rightly will reflect on you and Cllr Carter. We pay you to repesent

us. You should be questioning this errant £5 million.

The CPO issue is simply a massive cover-

why they can't be open regarding this.

You should be exercising some sort of control over council officers, but

obviously councillors don't, and that is why we are getting the abuses that

are happening. I talk so many people who are so utterly disgusted by what

is going on they are determined to change things.

We shall see how it all pans out and you are right, I won't wait till the

end of the week. I am a bit disappointed that the Express didn't print my

letter about your bottom -

Kind regards

Mrs Oliver

-

From: "Cllr Mark Weldon" <cllr.mark.weldon@stockport.gov.uk>

To: "sheilaoliver" <sheilaoliver@ntlworld.com>; "FOI Officer"

<foi.officer@stockport.gov.uk>

Cc: "Cllr Mark Weldon" <cllr.mark.weldon@stockport.gov.uk>; "John Hill"

<john.hill@stockport.gov.uk>

Sent: Tuesday, March 11, 2008 7:57 PM

Subject: RE: CPOs Harcourt Street

Dear Mrs Oliver,

Freedom of information decisions are not part of the political arena. FOI is

therefore not my "area of responsibility ".

As I'm sure you will agree it would be most inappropriate for politicians to

make such decisions so please don't wait until the end of the week.

Yours

Mark Weldon

-

From: "sheilaoliver" <sheilaoliver@ntlworld.com>

To: "FOI Officer" <foi.officer@stockport.gov.uk>

Cc: "Cllr Mark Weldon" <cllr.mark.weldon@stockport.gov.uk>; "John Hill"

<john.hill@stockport.gov.uk>

Sent: 11/03/08 18:54

Subject: CPOs Harcourt Street

Dear FOI Officer

I notice you persist in your illegal action in withholding the Harcourt

Street CPO background documents. There can be no justification for

withholding the background CPO documents, emails etc; this demonstrates the

Council's wish for ridiculous and inappropriate levels of secrecy.

Given today's press questioning and the public interest in the story, unless

I am allowed to view all the documents by the end of this week, this matter

shall be brought up in the local press.

It is Cllr Weldon's area of responsibility; he purports to be all in favour

of the FOIA. It will make him look a little bit (more) iffy in the run up

to the local elections. Do we want that? No, we don't!

Looking forward to hearing from you.

Sheila

-

From: "sheilaoliver" <sheilaoliver@ntlworld.com>

To: "Cllr Mark Weldon" <cllr.mark.weldon@stockport.gov.uk>; "Leader" <leader@stockport.gov.uk>; "John Schultz" <chief.executive@stockport.gov.uk>; "Donna Sager" <donna.sager@stockport.gov.uk>

Sent: 10/07/08 08:05

Subject: Collapse in the building industry

Dear Sirs

Before signing any contract with a building contractor for the proposed school at Harcourt Street, some consideration must be given to the collapse in the housing market. This school is being partly funded by future housing sales. It would be negligent of SMBC and maladministration to commit to something so expensive at a time when a large part of the proposed funding for this scheme is no longer viable.

Kind regards

Sheila

-

From: sheilaoliver [mailto:sheilaoliver@ntlworld.com]

Sent: 16 July 2008 17:56

To: Leader; John Schultz

Cc: Cllr Mark Weldon; Donna Sager; Andrew Webb

Subject: Ha!

Dear Sirs

I note a 500 pupil school at Marple will cost £7.2 million. The Harcourt Street one is £10 million and rising fast. As we have said all along, it is too expensive.

It is a cross I have to bear always being right.

Kind regards and take care

Sheila

-

Dear Mrs Oliver

Thank you for your questions, in order to put them to the meeting can you identify which councillor they are be addressed to? The deadline for submission is 5.30pm.

Regards

For Democratic Services

From: Sheila Oliver [mailto:sheilaoliver@ntlworld.com]

Sent: 08 November 2012 15:57

To: Democratic Services

Cc: Cllr Sheila Bailey(EXT); Cllr David Sedgwick; Cllr Maureen Rowles; Cllr Tom Mcgee (EXT); Cllr Brian Hendley; Cllr Walter Brett; Cllr Tom Grundy; Cllr Colin Foster(EXT); Richard Coaton; Cllr Patrick McAuley; Cllr Sylvia Humphreys; Cllr William Wragg; Cllr Alanna Vine; Cllr Bryan Leck; Cllr Paul Bellis; Cllr Brian Bagnall; Cllr Linda Holt; Anthony O'Neill(EXT); Cllr Lisa Walker; Cllr Peter Burns(EXT); Cllr Adrian Nottingham; Cllr Kate Butler; Cllr Dean Fitzpatrick; Cllr Alexander Ganotis; Cllr A Verdeille; Cllr Wendy Wild; Cllr Chrisopher Murphy(EXT); Cllr Andy Sorton; Leader

Subject: Questions for the full council meeting

Dear Democratic Services

Questions for the full council meeting:-

1) in light of the SK Solution scandal, am I now allowed to question the NPS financial irregularities of circa £5 million at Vale View Toxic Waste Dump School?

2) Why are the payments probably being made to the owners of Offerton Precinct come December being kept secret? Surely protecting the commercial interests of such a company is now out of the question.

Kind regards

Sheila

Remember to use your vote in the elections for Police & Crime Commissioners which take place in each police authority area in England & Wales on Thursday 15th November 2012.

For further information about the Police & Crime Commissioners election visit www.stockport.gov.uk/elections or www.greatermanchesterpccelection.org.uk

Confidentiality:-

Checked by AVG -

Version: 2013.0.2742 / Virus Database: 2617/5880 -

-